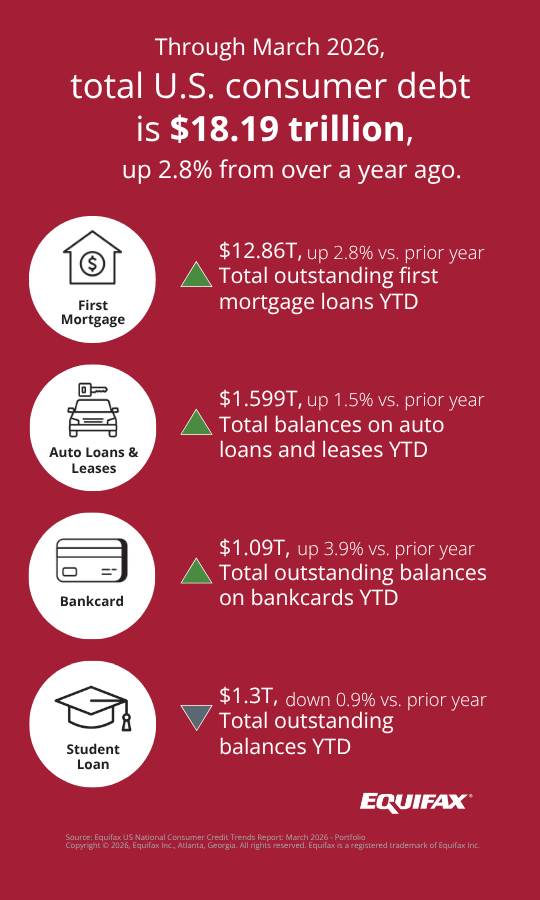

Americans now owe a record $18.19 trillion in consumer debt, according to new data from Equifax, and honestly, it is getting harder and harder to pretend everything is fine economically for regular folks.

The new report says much of the increase is being driven by credit card usage, especially among subprime borrowers. New bankcard accounts for subprime consumers jumped 18.6 percent year over year, while credit limits for those borrowers rose a whopping 37.6 percent. Revolving credit balances are also growing faster than inflation.

There is always going to be some finger pointing whenever debt numbers like this come out. And sure, some people absolutely make bad financial decisions. Some people overspend. Some people fail to save. That is reality. But another reality is that millions of Americans are simply struggling right now. Groceries are expensive. Rent is brutal. Insurance costs are absurd. Cars cost too much. Education costs too much. Even fast food feels overpriced these days.

For a lot of people, credit cards are no longer about buying luxury items or financing vacations. They are being used to survive.

ALSO READ: Americans fear recession while relying on credit cards to survive, says NerdWallet

That is why I think people should be careful about vilifying anyone carrying debt without knowing their story. A single medical issue, layoff, divorce, or family emergency can destroy someone financially in this country faster than many people realize. Once somebody falls behind, climbing back out becomes incredibly difficult.

Equifax described the current economy as “K-shaped,” and that honestly feels accurate. Some Americans are doing great. Others appear to be sinking deeper into debt just trying to maintain a basic middle-class life. Social media often hides that reality because people tend to showcase vacations, gadgets, and restaurant meals instead of maxed-out cards and anxiety.

The report also found that student loan delinquencies continue to rise. The 90-plus day delinquency rate reached 17.01 percent in March, marking the fourth consecutive monthly increase. Even though fewer student loans are being opened, borrowers are taking out larger amounts because college remains incredibly expensive.

Outside of student loans, delinquency rates on auto loans, personal loans, and bankcards improved slightly compared to last year. But lenders are simultaneously writing off more bad debt, especially in auto lending. That suggests banks are trying to clean up losses from consumers who already fell behind months ago.

Meanwhile, HELOC balances rose 13 percent year over year, which could mean homeowners are tapping home equity to stay afloat or consolidate debt. That is usually not a great sign either.

As someone who previously worked in banking for years, I can tell you that debt trends like this tend to reveal what people are experiencing before politicians or economists admit there is a real problem. When credit cards start becoming survival tools instead of convenience tools, something deeper is going on.

And unfortunately, $18.19 trillion in consumer debt feels less like a warning sign now and more like the new normal.

Support independent tech journalism

NERDS.xyz is independently owned and operated. If you enjoy my coverage of Linux, AI, hardware, cybersecurity, and tech culture, consider supporting the site on Ko-fi.

Support NERDS.xyz